Changing contours of competitive intensity in banks

29 Jan 2018

Executive summary

- The general public discourse and regulatory disposition towards the market structure of the Indian banking sector has flirted from consolidation to wider dispersion and back to consolidation in the last decade or so.

- We argue that the next stage is likely to be indifference, or possibly even irrelevance.

- Policy changes, hardening of regulation, expanding presence of non-banking channels and technology will continue to acquire greater significance for banks rather than the waxing and waning of competition that characterized much of the last twenty years.

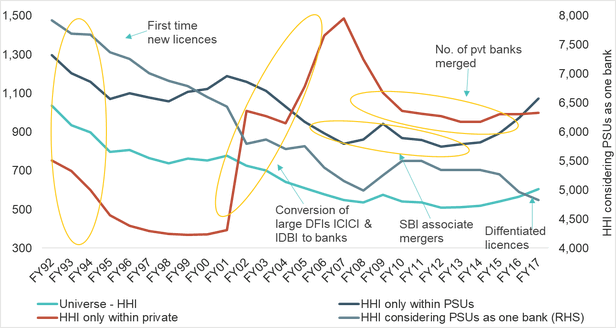

The competition was introduced for the first time through the award of ten new licenses for setting up of private sector banks in 1993-94. This did reduce market concentration1 rapidly, as a few of the new licensees expanded rapidly, even as they introduced products and technology that customers did not enjoy before. This continued well until the early 2000s, augmented also by conversion of the erstwhile ICICI Ltd to a bank. The next ten years were markedly different: there were a multitude of weak private banks exiting through mergers, the merger of two associates of SBI with itself, and only two licenses were awarded. Understandably, the angst against rising market concentration increased, culminating in another round of licenses being given out in 2015.

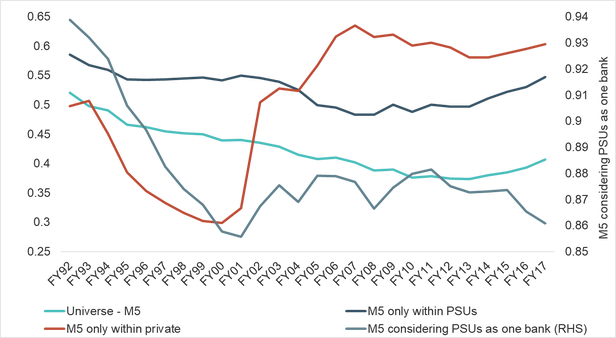

The M5 ratio2 broadly follows a similar pattern:

The simplistic history outlined above masks several nuances of the changes in the leitmotif of competition that banks need to be aware of for shaping themselves for the future.

First, a basic idiosyncrasy of the Indian banking market. Equally emphatic voices supporting competition and consolidation have co-existed. On the one hand, it is believed that banks don’t compete enough, and their net interest margins consequently are too high. On the other hand, some believe that we don’t need so many banks because they are clones of each other. On the face of it, the Indian banking market appears to be fairly competitive. As an example, according to the latest data available, Brazilian bank HHI was 1162 vs. India’s 604.

- The consolidation within PSUs, if and when it happens, will not change the competitive structure of the market unless they are made autonomous enough to aggressively compete within themselves first.

- Existing private lenders will have to worry about new “disruptions” rather than old-fashioned competition. And these, for example, a resurgent NBFC/HFC sector and fintech, will nibble at market shares. The excessive, “land grab” premium on a bank branch has collapsed and deposits are a much bigger challenge than when the likes of HDFC Bank got their licenses. If small new banks want to make a competitive pitch, they will have to devise ways of acquiring deposits in scale at a lower cost, and thereafter continue to service them at lower operating costs.

- Policymakers have made it clear that whereas increasing competition was their explicit stated motive in the 1990s, it is not so any longer – fostering financial inclusion is. And the Jan Dhan and Mudra experiments, inter alia, have proved beyond doubt that financial inclusion can be, and must be, furthered through innovative means rather than increasing the number of banks, just as it is not necessary to have more pharma companies for medicines to reach more villages. By implication, existing private banks will have to do their bit of heavy lifting on financial inclusion (not new but likely to accelerate), but at substantially lower than the unaffordable cost structures at present.

- 1 We use two measures of market concentration –

i) The simple five-firm concentration ratio – M5 – or the sum of the market share of the top five banks ii) The more robust Herfindahl Hirschmann Index – HHI – which is the sum of squares of the market share of all banks in the set, multiplied by 10,000. As a thumb rule, an M5 of 0-40% indicates low concentration, 40-70% high concentration and 70%+ a near-monopoly. An HHI of less than 1,500 is considered a competitive marketplace, 1,500-2,500 moderately, and > 2,500 a highly concentrated marketplace.

- 2 For the sake of uniformity, all ratios are for banks’ total assets. For many banks and/or years, loans and deposits were separately not available. Indian banks’ data is for 1992-2017.

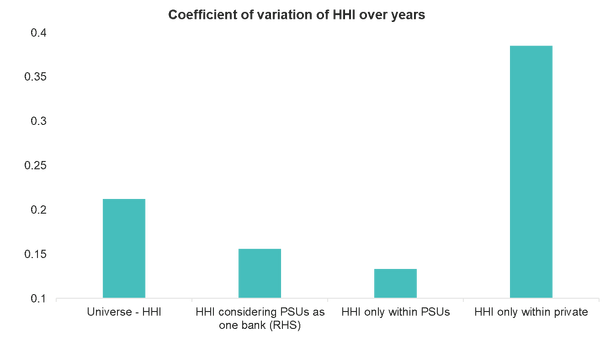

- 3 Standard deviation divided by the mean, a measure of variability.