When the tide turns: How VCs can sail through the rough seas of MEA market?

12 Oct 2023

The MEA economy was largely insulated from

global headwinds in 2022 supported by high oil prices and strong balance sheets

at the sovereign and corporate levels. However, slow-down in growth was seen in

H1 2023 and is expected to continue next year as well. Tight fiscal and

monetary policies which had been implemented to fight inflation and reduce

vulnerabilities have begun to impede economic activity in many countries.

Moreover, oil production cuts have curbed growth in oil exports which remains

as one of the major source of income for MEA countries.

Current

inflation in the Middle East at ~14% and Africa at ~16% has been higher than pre-COVID

levels of 5% and 9% in 2019 respectively leading to reduced purchasing power

and higher borrowing costs, making investments riskier and diminishing VC

funding. Additionally, higher interest rates, exceeding 5%, have made it more

challenging for start-ups to borrow capital.

MEA’s

VC market is widely considered as a bloc, however it is quite dynamic in terms

of the venture investing landscape which is comprised of three groups of

countries. The first group of countries (Qatar, Kuwait, and other oil-rich

countries) are “resource-rich” attributed to their small population size and

small geographical expanse yet significant, resource-driven GDPs. The second

group of countries (like Egypt, South Africa and Kenya) are classified as

“promising prospects” because of their young, large and growing tech-savvy

populations. The third group of countries are considered to be “amalgamated

markets” including the likes of United Arab Emirates (UAE) and the Kingdom of

Saudi Arabia (KSA) which are endowed with plentiful capital, land, and population.

- 2021

and 2022 witnessed a substantial increase in venture capital funding in the

region, propelled by governmental backing, legal and regulatory reforms, as

well as advancements in privatization and infrastructure development.

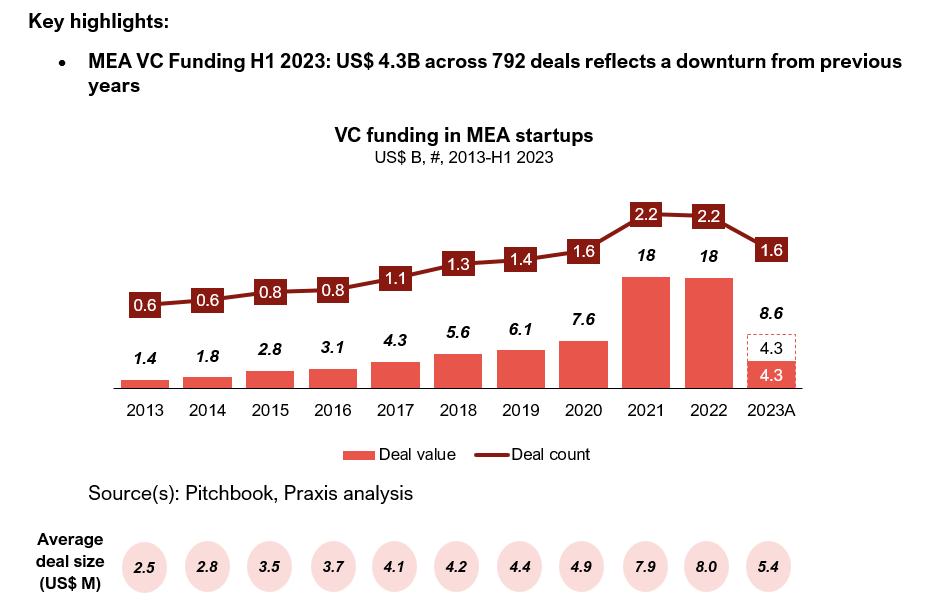

- Weakness

due to high inflation and interest rates caused liquidity constraints in MEA

market, leading to a significant decline in VC funding during H1 2023, with a

51% YoY decrease compared to H1 2022.

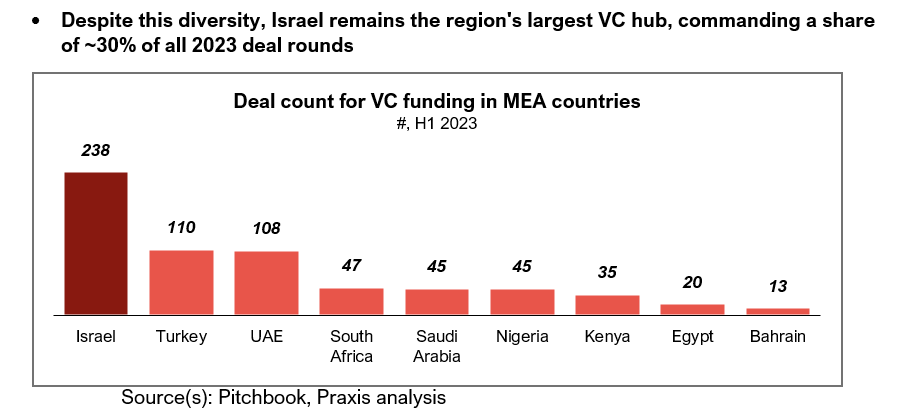

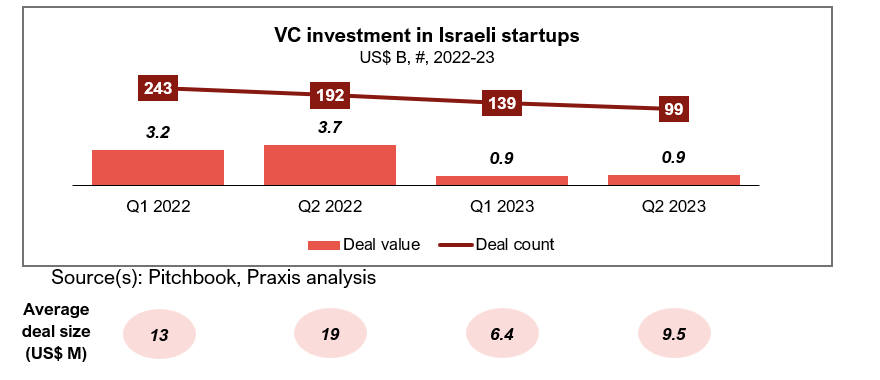

- Number

of Israel’s start-up deals decreased by 45%, compared to a global drop of 34%

amplified by rising concerns over country’s judicial system overhaul that

impacted investor confidence in tech ecosystem.

- Despite

a 27% YoY decline in VC deal value in H1 2023, Saudi Arabia’s growing

prominence, owing to reforms driven by Saudi Vision 2030, is evident as it

pipped past UAE in deal value with US$ 446M VC funding in H1 2023 on back of

two mega deals worth US$ 289M (by e-commerce start-ups Floward and Nana).

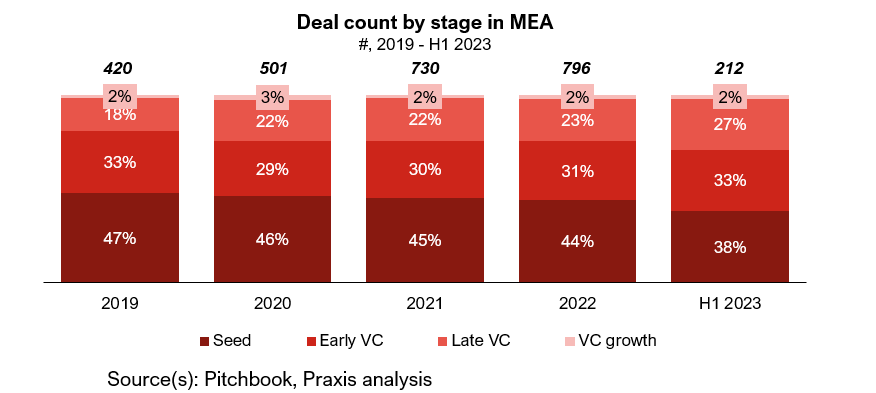

- Shift

towards late-stage deals attributed to increase risk aversion amidst weak

macro-economic situation and concerns regarding portfolio returns

- Supported by policies like free economic zones, tax laws, and government support for technology and digitization, MEA’s entrepreneurial ecosystem has seen a rise over the years; Israel’s Tel Aviv ranks 10th in Global Start-up Ecosystem Index 2023

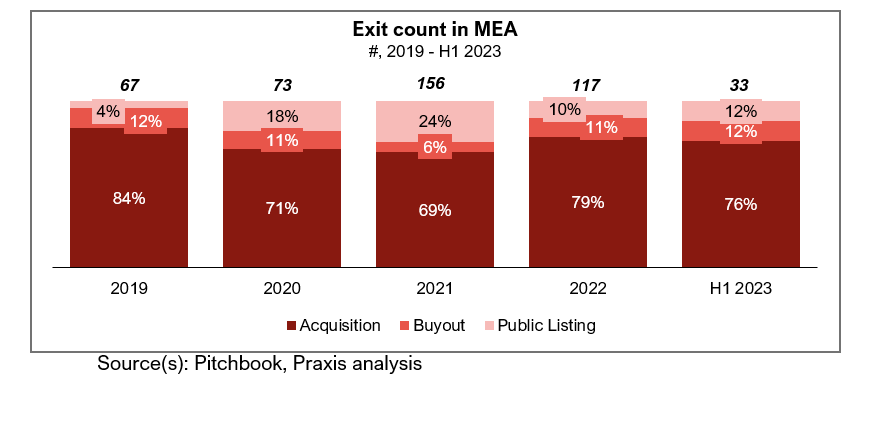

- Exit activity remains muted with 33 exits reported in MEA during H1 2023, 50% YoY reduction

- Muted exit options, owing to

tighter funding conditions and low valuations, are leading to longer asset

holding periods causing VCs to focus on growth and stability of existing

portfolio companies to ensure maximum value extraction

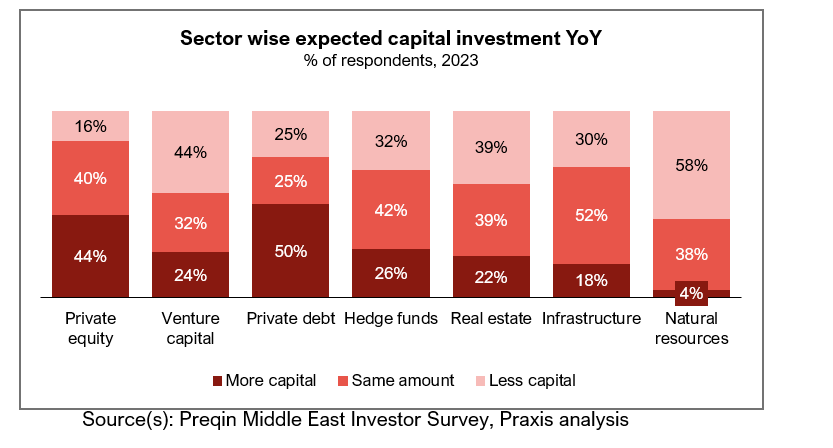

- Survey:

Positive investor outlook towards late stage investing with a rebound in early-stage investing expected in

line with global trends

– According to Preqin survey, 46% of investors in

the MEA region believe that VC funds have not met their expectations and are

cautious due to concerns about their performance and returns

- Investors

keen to invest more in high value-less risky funds; 84% of those surveyed

willing to maintain / increase exposure to private equity.

Implications for VCs in the

MEA region

- High risk, high reward:VCs need to be aware of the unique set of challenges and opportunities that exist in the region. Although, MEA has historically been prone to economic and political instability along with currency risks, there has been a growing number of success stories backed by increasing availability of capital, favourable demographics and rising internet penetration

Patience is key:Low asset valuations amidst this economic downturn and spiralling inflation has opened up new investment opportunities for VC investors. However, VCs are advised to be to be patient and take a long-term view when investing in start-ups to maximise returns

Survival of the fittest: VCs need to be selective when choosing which start-ups to invest in. Even though venture VC as an asset class is one of the most exposed to the current market turmoil, 2023 may prove to be instrumental in assessing the performance of these start-ups

How can investors prepare?

Ear to the ground: MEA is a relationship-driven region where a local presence is important to start-up founders who value trust and availability. With a local presence, investors can be cognizant of the ever-changing market conditions. Some of the most active global funds already have local presence in MEA with an office or a partner in the region

Practice caution: Investors are advised to proceed with caution in times of adversity. Due-diligence start-ups to maintain high selectivity while choosing start-ups to fund with a focus on Commercial DDs and Founder DDs

Deepen domestic expertise: Investors can help start-ups navigate around the regulatory nuances of the region via exposure to investor portfolio companies, access to local customers and access to existing commercial and banking licenses

Build international network: Access to a global network of clients experts and talent is of immense value to start-ups, especially those looking to scale internationally or having with nuanced staffing and skills requirements or global potential

On a final note…

The MEA region has experienced the impending downturn in VC funding in H1 2023 with a 51% YoY dip in funding and is likely to continue till 2024. While “amalgamated markets” like Saudi Arabia and “resource-rich” countries like Bahrain and Qatar driven by government initiatives have shown resilience, “promising prospects” like Israel have seen a substantial decline.

Despite facing a challenging landscape marked by uncertainties, tighter funding conditions and reduced exit activity, MEA’s start-up ecosystem is resilient and evolving. The increasing maturity of the start-up ecosystem, reflected in a rise in late VC deal counts, signifies a robust foundation. The combination of this strong foundation combined with supportive government policies and growing digital savvy population will pave the way to unlock the untapped potential of the MEA venture market making the next four to five years monumental in defining MEA as the next hotspot for VC investors.Akshat Gupta

Practice Leader- Private Capital

Praxis Global Alliance