India’s E-Bus Boom - Why is it going electric

21 May 2025

India is witnessing a silent revolution in

public transport. While headlines focus on electric cars and two-wheelers, it’s

the electric bus (E-bus) that is making serious strides across cities. As state

transport undertakings (STUs) and private operators expand their fleets, the

real question is: why are E-buses gaining such traction, and will this boom

sustain?

What’s driving the E-Bus boom?

India’s urban public transport is under pressure to

decarbonize, reduce operational costs, and modernize service quality. Electric

buses check all three boxes. Backed by policy mandates, declining battery

costs, and favourable TCO dynamics, E-buses are now a central pillar of India’s

clean mobility strategy.

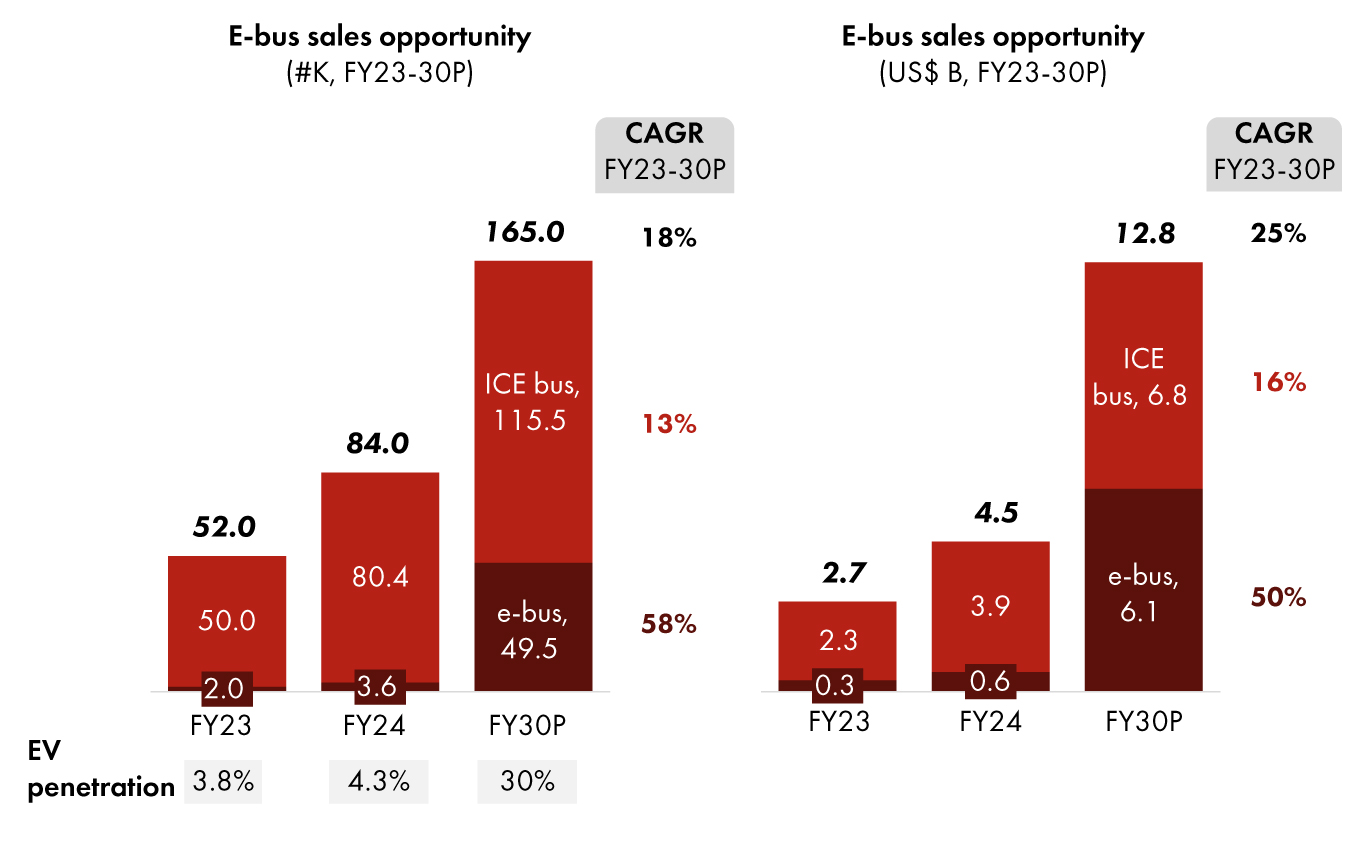

How big is the market?

Exhibit 1: E-Bus Market Size

and Penetration in India (FY24 vs. FY30)

Most of this growth will come from intra-city buses,

given their predictable routes and depot-based operations. Inter-city and

long-haul electrification will remain limited in the near term due to range and

charging constraints.

Why is TCO the game-changer?

The total cost of ownership (TCO) for E-buses is increasingly favorable, especially when supported by incentives and high asset utilization. Compared to diesel buses, E-buses save on energy consumption and maintenance, with lifecycle savings of up to 7-10%.

Exhibit 2: TCO Comparison:

Electric vs. diesel buses

Moreover, cities are exploring innovative deployment

models, such as public-private partnerships, leasing, and battery-swapping, to mitigate upfront costs and enhance uptime.

What are the expansion plans of OEMs?

E-bus manufacturers are expanding their portfolios and domestic

manufacturing capacities in direct response to rising EV-specific demand from

governments across India. This strategic alignment with public procurement

needs is shaping product innovation, capex allocation, and operational models.

Companies such as Tata Motors, Eicher, PMI

Electro Mobility, Olectra, Switch Mobility, JBM Auto, etc, are introducing new electric

and alternative fuel bus variants, investing in manufacturing

infrastructure, and enhancing R&D capabilities.

Several players are securing large public contracts, while others are forming partnerships and scaling up production to meet state-level electrification targets. Together, these OEMs are positioning themselves to serve a fast-growing market driven by central schemes and state-led transport electrification programs.

Challenges to watch out for?

Despite growing momentum in E-bus adoption, several persistent challenges continue to affect the pace and scale of deployment. These span financial constraints, infrastructure limitations, and operational hurdles that particularly impact public transport agencies and state-led programs. As the ecosystem evolves, addressing these issues is critical to unlocking mass adoption and long-term viability.

However, with over 25 states drafting or

implementing EV policies and nearly 10,000 buses sanctioned under central

schemes, the ecosystem is actively maturing.

What should stakeholders do?

- OEMs need to localize production and innovate on modular, fast-charging buses

- Infra providers must accelerate depot electrification and megawatt-level charging hubs

- STUs must leverage central schemes to transition rapidly to electric fleets via opex models

- Private operators should explore leasing models and B2G contracts in smart cities

Conclusion

India’s E-bus story is not just about replacing diesel

buses – it is about building a future-ready, sustainable public transport

system. With economics turning favorable and policy support strong, the E-bus

boom is here to stay. Stakeholders who invest early, build scale, and integrate

across the value chain will lead the charge.

For a deeper dive, refer to the full report- Electrify30: The Future of Mobility