Smarter branch operating models: Designing future-ready branch strategies

15 Jul 2025

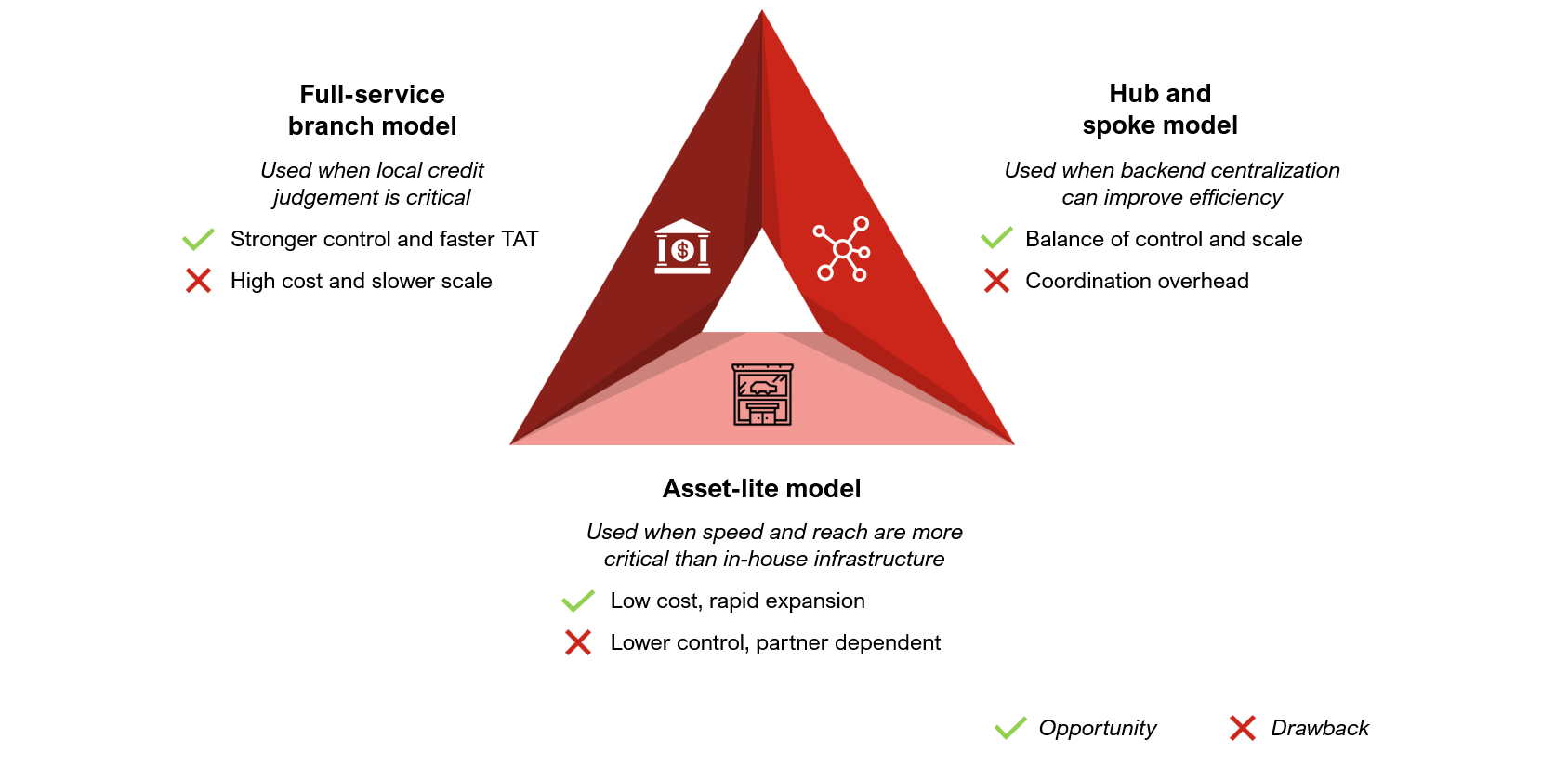

2.1 Full-service branch model:

2.1 Full-service branch model: 3. Structuring branch functions to improve productivity

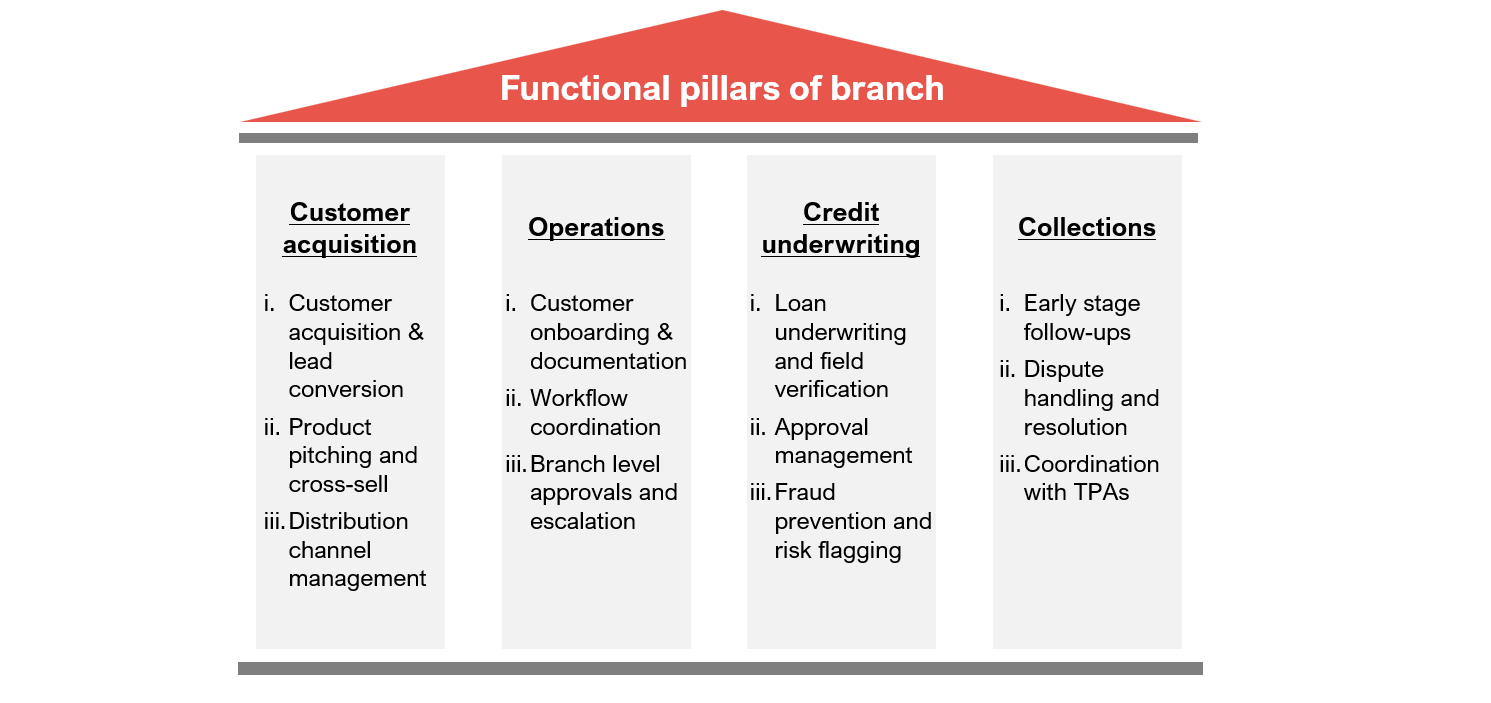

With the operating model in place, the next focus is on how key branch functions are structured for performance. Branches are built around four critical functional pillars: Customer acquisition, operations, credit underwriting, and collections. Each of these must be clearly structured to enable faster decision-making, accountability, and consistency across markets.

Exhibit 2: Four critical pillars of a branch

3.1 Customer acquisition: Sales teams drive

customer acquisition, and their design must match the market’s pace and profile

to ensure both agility and cost efficiency.

3.1 Customer acquisition: Sales teams drive

customer acquisition, and their design must match the market’s pace and profile

to ensure both agility and cost efficiency.In-house DSTs offer better control and lead quality, especially in high-volume markets, though they come with higher fixed costs. DSAs and local connectors help expand reach in rural and semi-urban markets at lower fixed costs, but offer limited control on lead quality. Sales structures vary by geography, with metro branches often operating leaner, DST-heavy setups, while rural branches rely more on external partners for wider reach.

Can Fin uses a blended model, with ~50% of sourcing through DSAs and rest via in-house DSTs, whereas HFFC relies entirely on external channels such as DSAs and connectors for originations.

3.2 Operations: Branch operations must be designed to prevent service delays and ensure efficient branch throughput.

Defined spans of control help avoid managerial overload, strengthen the frontline, and improve overall effectiveness. Clear reporting structures reduce ambiguity and enable faster issue resolution through timely escalations. Function-wise task allocation minimizes duplication and ensures a smoother, more streamlined service flow.

3.3 Credit underwriting: Efficient credit workflows improve TAT without compromising underwriting standards. Branch credit functions must be clearly defined and empowered.

AI-led Business Rule Engines (BREs) enable instant approval of smaller loans, freeing up manual bandwidth for complex cases. For instance, L&T Finance’s Project Cyclops uses AI and alternate data, including geolocation, to underwrite first-time borrowers and has improved new-to-credit (NTC) loan approvals by 34%. To maintain risk control, approval limits are tiered by ticket size and borrower credit history, while high-value or complex loans are routed to central teams for additional scrutiny.

3.4 Collections and recovery:

Effective collections require speed in early stages and scale as delinquencies rise.

Early-stage follow-ups are handled in-branch to preserve customer relationships and enable faster resolution. After defined delinquency threshold limits, Third-Party Agencies (TPAs) can be involved to take over recovery. This phased approach allows internal teams to focus on relationship-led collections in early buckets, while agencies take over higher-volume, late-stage buckets more aggressively.

Religare Finvest Limited (RFL) deployed FinnOne mCollect solution, achieving ~90% field penetration and per-receipt cost came down to 30% of prior expenses.

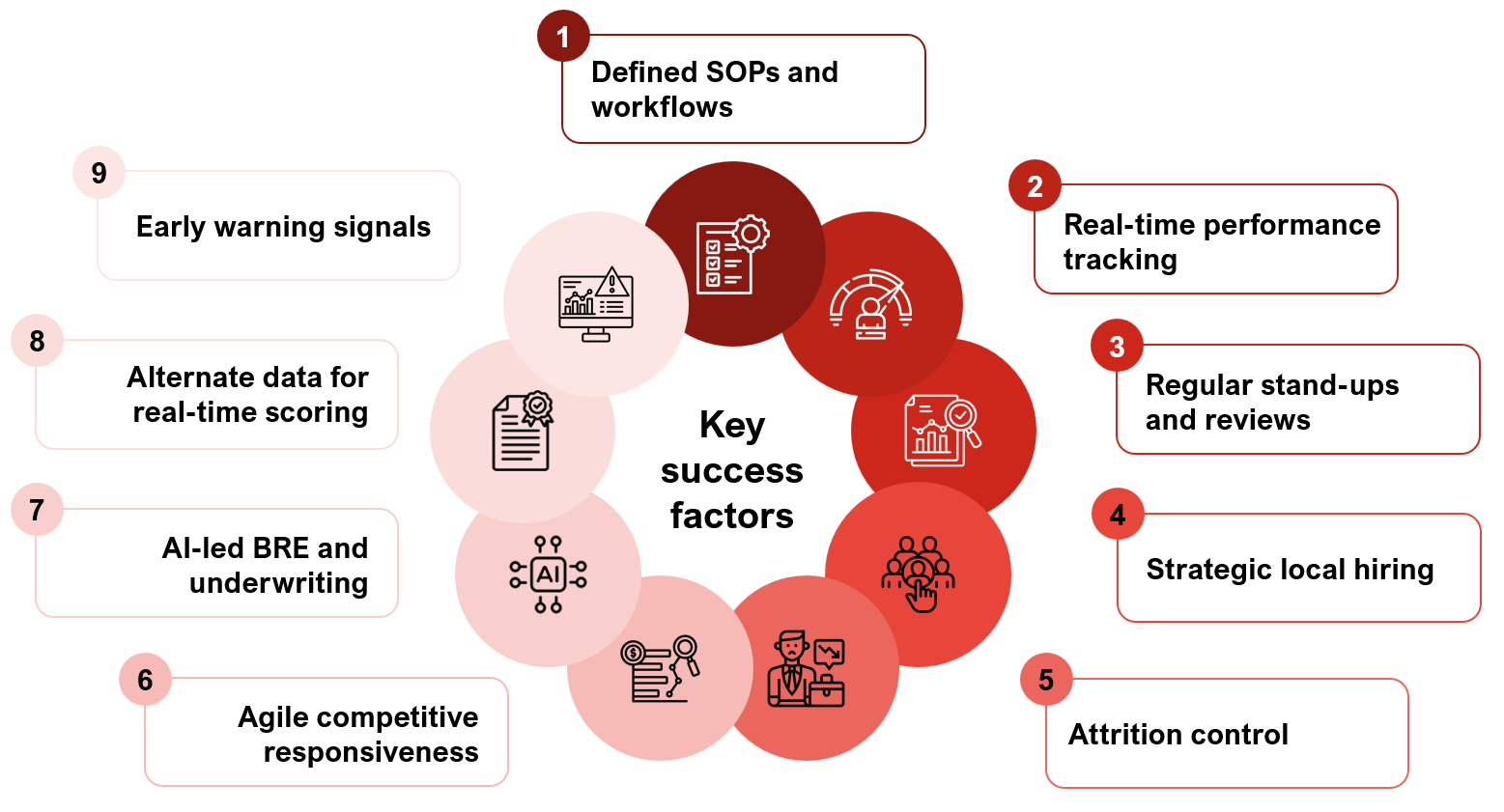

4. Key success factors driving branch productivity

Sustainable branch performance across functional pillars depends on operational discipline. By combining process standardization with agile execution, NBFCs can ensure faster service, fewer errors, and stronger customer experience.

Exhibit 3: Key success factors that drive branch productivity

5. Conclusion: Smarter branch ops for scalable impact

The future of branch-led growth lies not just in expanding headcount or square footage, but in building lean, responsive, and tech-integrated operating models. Leading NBFCs are adopting fit-for-purpose operating models, structuring key functions for speed and accountability, and embedding process discipline with real-time performance tracking. Branches that balance autonomy with central oversight, hire and retain the right talent, and follow standardised yet agile workflows are better placed to scale sustainably.

To stay competitive, NBFCs must rethink their branch operating playbook, designing branches as modular, data-enabled units that deliver speed without compromising control. Retaining the right talent is critical, as new hires often take 6-8 months to operate at full potential, making churn a hidden cost. It’s not about doing more but doing it smarter.

6. Design your branch strategy with Praxis

Exhibit 4: Capabilities we build and implement