Opportunities across the Genomics value chain

12 Jun 2025

Investment and cost background:

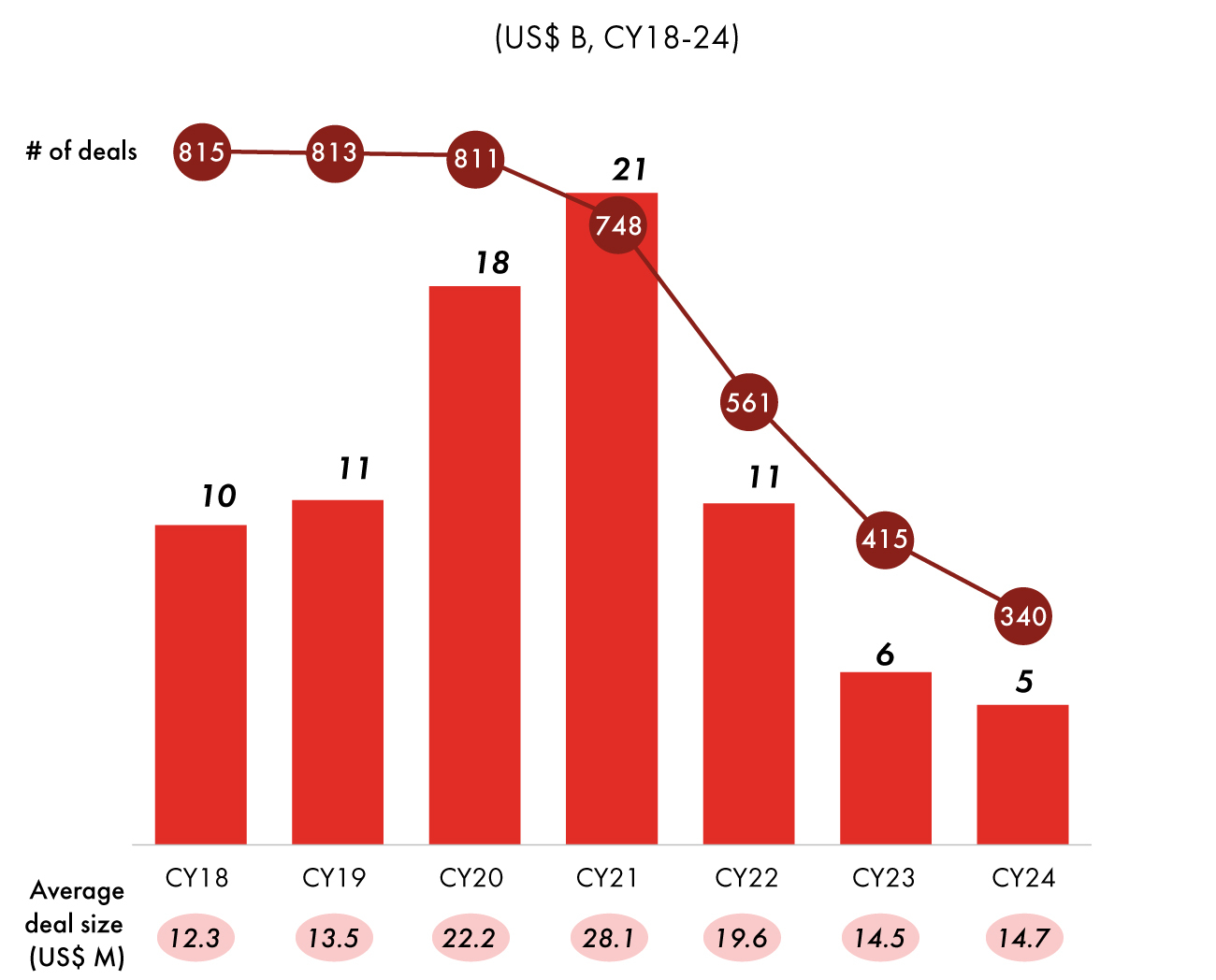

Globally, the genomics industry has attracted significant investor interest over the past few years, with funding levels peaking at US$ 21B in CY21 and remaining structurally higher than pre-CY20 levels (Exhibit 1).

Exhibit 1: Global genomics y-o-y funding amounts and # of deals

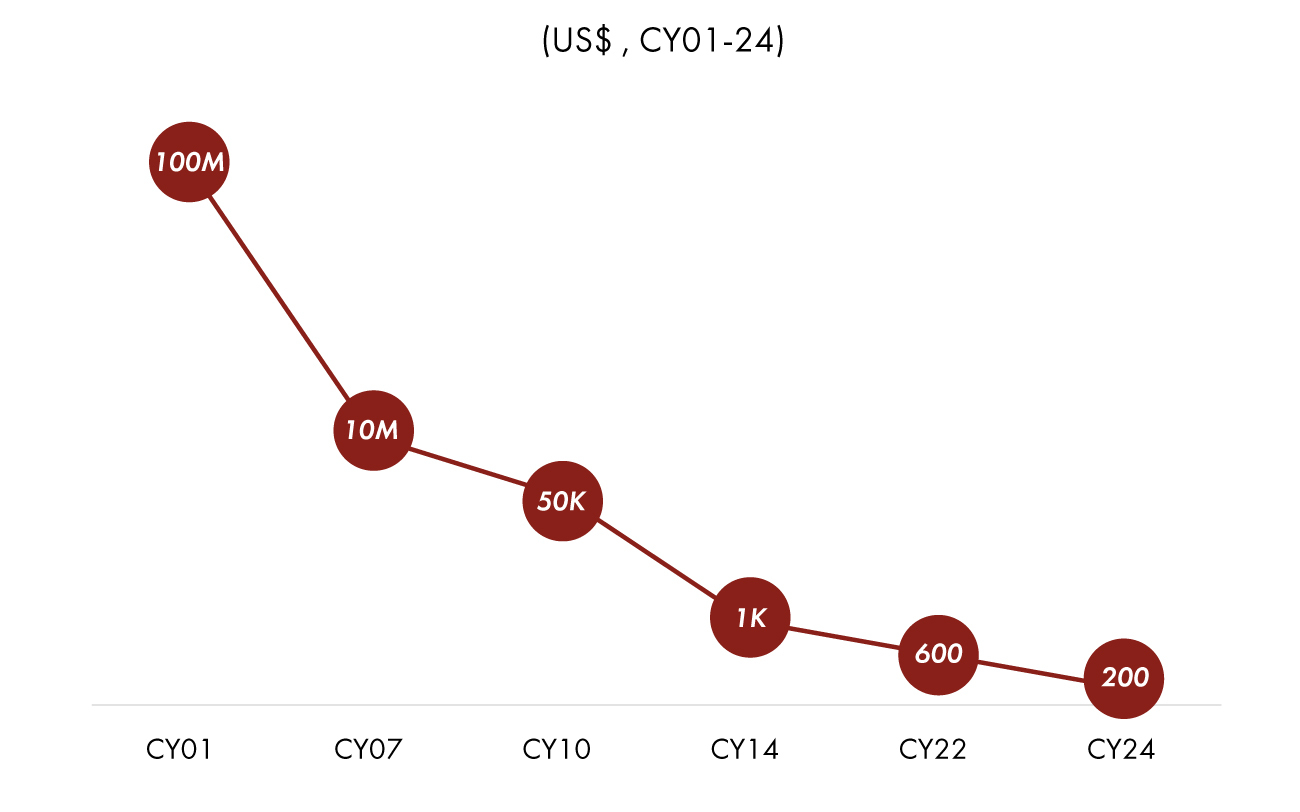

At the same time, the cost of sequencing a human

genome has fallen precipitously from nearly US$ 100M in 2001 to under US$

200 today (unlocking access to genomic data at an unprecedented scale) (Exhibit

2).

Exhibit 2: Sequencing costs per genome

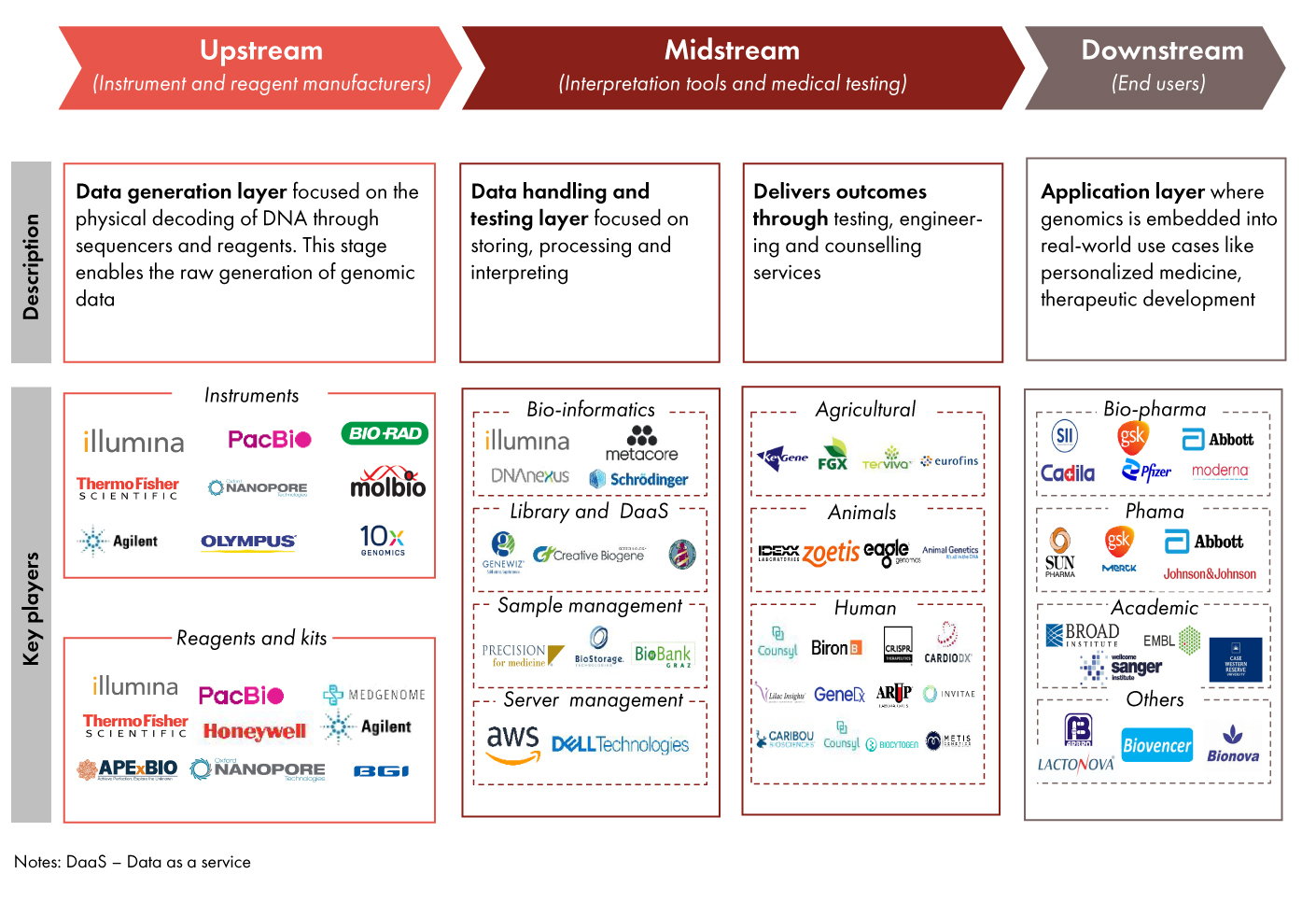

The genomics value chain:

The genomics value chain comprises three core layers: upstream, midstream, and downstream (Exhibit 3), each playing a distinct role:

- Upstream refers to the data generation layer, involving manufacturers of sequencing instruments, reagents, and kits that enable large-scale DNA decoding

- Midstream includes two parts:

- Infrastructure storage and analytics: Platforms that store, process, and interpret genomic data through bioinformatics, cloud tools, and AI-based analytics

- Testing counselling and therapeutics: Providers that deliver genetic testing, risk profiling, and counselling across human, animal, and agri-health context

- Downstream, the application layer, where genomic insights are deployed in drug development, precision medicine, agriculture, and academic research

Opportunites across the value chain:

The genomics value chain encompasses a variety of business models and companies tailored to the specific function of each segment upstream, midstream (infrastructure and diagnostics), and downstream applications. Upstream players rely on bundled hardware and consumables, midstream infrastructure operates on SaaS and data access models, while diagnostic and therapeutic developers focus on licensing, partnerships, and outcomes-based pricing. As the ecosystem matures, each segment is evolving distinct commercial levers to scale sustainably. A detailed breakdown of these models and opportunity areas is provided in Exhibit 4.

Exhibit 4: Opportunities across the value chain

Conclusion:

As the genomics ecosystem moves from early discovery to real-world deployment, commercial models are evolving across every layer of the value chain. What began in academic labs is now led by product-driven companies, modular platform providers, data monetization engines, and IP-led innovators. With sequencing becoming more accessible, analytics and storage infrastructure maturing, and monetization models diversifying from SaaS-based analytics to D2C wellness and dataset licensing, genomics is set to become a foundational pillar of innovation across healthcare, agriculture, and industry. Stakeholders who can align product strategy with scalable, monetizable use cases will be best positioned to lead this next wave of genomics-driven growth.