What's next in diagnostics

19 May 2025

The field of medical diagnostics is experiencing unprecedented innovation, moving rapidly beyond traditional methods towards approaches that are more precise, predictive, and patient-centric, particularly in developed markets across North America, Europe, and Asia-Pacific. This transformation is driven by a powerful convergence of advanced biological understanding, sophisticated data science, and cutting-edge engineering.

Diagnostics transforming healthcare

The diagnostics sector is undergoing a seismic

shift, powered by disruptive technologies, digitalization, and intelligent

automation. This evolution creates a new diagnostic paradigm impacting how

healthcare systems operate, diagnose, and manage diseases. This emerging set of

diagnostic tests is shaped by several cross-cutting themes that are redefining

clinical practice and patient care:

- Demand for non-invasiveness: Patient preference and clinical benefits are spurring the adoption of non-invasive techniques, opening markets previously reliant on invasive procedures

- AI and automation: Artificial intelligence is boosting speed, accuracy, and workflow efficiency, creating value through cost savings and improved outcomes

- Early detection focus: A shift towards early detection and prevention aims to reduce long-term healthcare costs and disease burden, creating demand for screening technologies

- Decentralization: The move towards point-of-care and at-home testing expands market reach beyond centralized labs

- Precision medicine: Omics-driven and biomarker-based approaches are enabling precision diagnostics tailored to individual biology

The

diagnostic revolution: 10 tests to watch

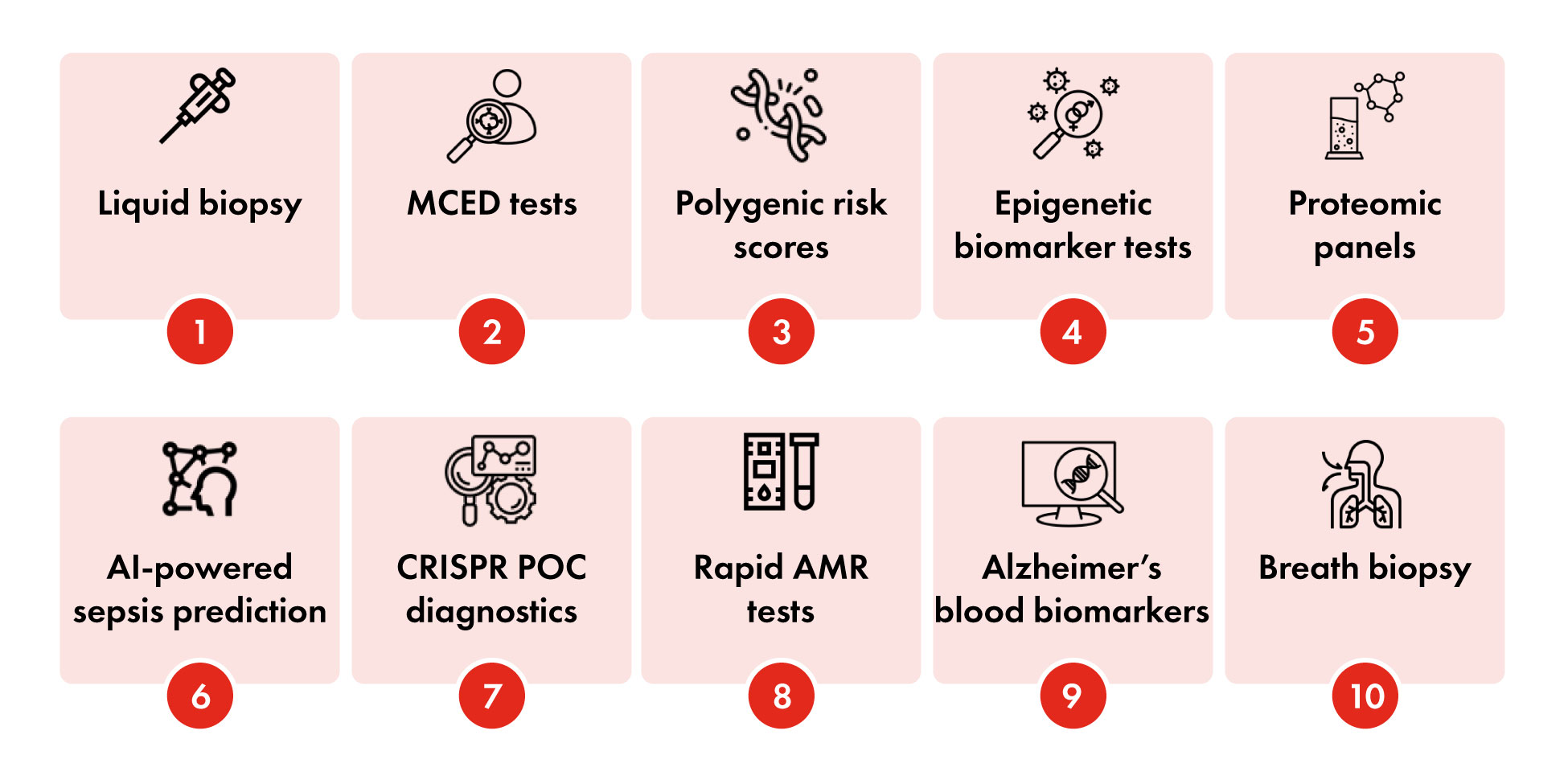

1. Liquid biopsy

- Market: US$ 10.9B (Global), US$ 5.1B (USA), US$ 0.8B (UK), US$ 0.3B (India)

- Purpose/problem solved: Enables cancer detection and monitoring via blood/fluid analysis, reducing reliance on invasive surgical biopsies

- Key differentiator: Minimally invasive, allowing frequent monitoring and insights into tumor evolution

- Current adoption & scale: Clinical adoption is rapidly expanding, particularly in US oncology for treatment selection and monitoring. Global scale is substantial and growing; Indian adoption is nascent but accelerating

- Adoption drivers: Rising cancer prevalence (~20M global new cases annually, projected to reach 35M by 2050), demand for non-invasive methods, personalized medicine focus

- Commercial hurdles: Need for consistent testing methods across labs/platforms so doctors can reliably compare results; achieving high sensitivity for detecting trace amounts of cancer

- Future potential: Addresses millions of annual global cancer cases, indicating transformative potential in cancer care

2. Multi-cancer early detection (MCED) blood test

- Market: US$ 1.2B (Global), US$ 1.1B (USA), US$ 50M (UK)

- Purpose/problem solved: Aims for early detection of multiple cancers via a single blood test in asymptomatic individuals, targeting cancers without established screening methods

- Key differentiator: Pan-cancer screening capability from one blood sample

- Current adoption & scale: Available as Lab Developed Tests (LDTs) with ongoing large-scale clinical validation studies (e.g., NHS-Galleri trial in the UK involving 140,000 participants). Early commercial rollout in the US with growing physician and payer interest. No FDA approvals yet

- Adoption drivers: Addresses major unmet need in early cancer detection, potential to improve survival

- Commercial hurdles: Gaining regulatory approval (e.g., FDA); securing broad insurance coverage; ensuring very high accuracy to minimize patient anxiety from false positives; establishing clear and efficient diagnostic follow-up procedures

- Future potential: Targets the vast population eligible for cancer screening. Addresses the majority of cancer deaths occurring from types without routine screening. Represents a paradigm shift, contingent on overcoming commercialization barriers

3. Polygenic risk scores

- Market: Currently in its nascent stage and ready for clinical adoption

- Purpose/problem solved: Estimates inherited genetic risk for common complex diseases (cardiovascular, diabetes, etc.) to guide personalized prevention

- Key differentiator: Assesses risk based on numerous common variants, applicable broadly across populations

- Current adoption & scale: Primarily utilized in direct-to-consumer offerings and research settings; clinical adoption remains limited

- Adoption drivers: Growing interest in personalized/preventive health, potential to refine risk assessment beyond traditional factors (e.g., lifestyle, age)

- Commercial hurdles: Need to prove consistent accuracy across diverse global populations (current data often Eurocentric); making results easily understandable and actionable for non-specialist clinicians

- Future potential: Targets highly prevalent chronic diseases causing >60% of global deaths. Significant potential for impact if effectively integrated into routine primary care

4. Epigenetic

biomarker tests

- Market: US$ 10.1B (Global), US$ 5.3B (USA)

- Purpose/problem solved: Detects early molecular changes—specifically DNA methylation patterns, which are the locations and levels where methyl groups (–CH3) are added to the DNA—linked to diseases like cancer, cardiovascular disorders, and neurological conditions, enabling earlier and more accurate diagnosis than traditional genetic or imaging tests

- Key differentiator: Provide sensitive, minimally invasive detection of dynamic gene regulation changes linked to real-time disease activity, enhanced by AI for improved accuracy beyond static genetic tests

- Current adoption & scale: Clinical adoption is growing rapidly, particularly in oncology for early cancer detection, prognosis, and treatment monitoring, FDA approved with substantial adoption in North America and Europe

- Adoption drivers: Rising prevalence of chronic diseases globally, aging populations, increasing investment in epigenetics research and precision medicine, and technological advances in sequencing and bioinformatics

- Commercial hurdles: Complexity in interpreting epigenetic data along with high costs of advanced assays

- Future potential: Positioned to revolutionize early disease detection and personalized medicine by enabling dynamic monitoring of disease progression and treatment response

5. Proteomic panel testing

- Market: US$ 27.8B (Global), US$ 11.2B (USA), US$ 1.3B (UK), US$ 1.0B (India)

- Purpose/problem solved: Analyzes large sets of proteins for deep biological insights, aiding early disease detection, monitoring, and drug discovery

- Key differentiator: Dynamic view of health status, potential for novel biomarker discovery, complements genomics

- Current adoption & scale: Significant scale in research; clinical diagnostic adoption is emerging

- Adoption drivers: Technology advancements, personalized medicine demand, R&D investment

- Commercial hurdles: High cost of analysis platforms limits broader clinical access; significant challenge in translating complex protein data into clear, actionable clinical recommendations; requires extensive validation studies

- Future potential: Targets major chronic diseases. Key enabler for precision medicine

6. AI-powered sepsis prediction

- Market: AI engagement in sepsis is still in its early stages

- Purpose/problem solved: Uses AI on EHR data to predict sepsis risk earlier than clinical signs, aiming to improves survival and reduce intensive care needs

- Key differentiator: Automated, continuous monitoring for early risk identification, potentially hours before symptoms escalate

- Current adoption & scale: Low clinical implementation volume; largely in validation/pilot phases

- Adoption drivers: High sepsis mortality and associated healthcare costs (~50M global cases annually); potential for major impact on patient outcomes

- Commercial hurdles: Difficulty integrating seamlessly with diverse hospital IT systems; need to build clinician confidence and trust in AI recommendations over traditional judgment; proving clear cost-benefit in real-world settings

- Future potential: Addresses a leading cause of hospital deaths globally. Potential to significantly improve outcomes for millions of patients if tools prove robust and integrable

7. CRISPR-based Point-of-Care diagnostics

- Market: US$ 4.3B (Global)

- Purpose/problem solved: Leverages CRISPR precision for potentially rapid, low-cost, portable molecular tests usable outside central labs

- Key differentiator: High specificity, potential for simple field deployment, adaptability to new targets

- Current adoption & scale: Minimal clinical volume; usage is primarily in R&D settings

- Adoption drivers: Need for decentralized/rapid infectious disease testing (pandemic preparedness), potential for lower cost vs traditional labs

- Commercial hurdles: Simplifying sample preparation for non-expert use; ensuring reagents are stable without refrigeration; achieving low production costs for affordability; navigating regulatory approval for POC settings

- Future potential: Could democratize advanced molecular diagnostics, making rapid, portable testing available even in low-resource settings, transforming global disease detection and outbreak management

8. Rapid molecular tests for antimicrobial resistance (AMR)

- Market: US$ 4.8B (Global)

- Purpose/problem solved: Quickly identifies antibiotic resistance, enabling faster appropriate treatment and combating the AMR crisis

- Key differentiator: Speed (results in hours vs days for culture)

- Current adoption & scale: Growing use in hospitals, particularly in developed countries. Point-of-care options are expanding but adoption is limited by price

- Adoption drivers: Urgent global threat of AMR (~5M associated deaths globally); critical need for faster results to optimize treatment and preserve antibiotic effectiveness

- Commercial hurdles: High cost of testing systems and consumables limits access, especially outside high-resource settings; requires integration into hospital workflows

- Future potential: Addresses a critical global health threat. Essential tool for modern infection management; strong growth expected

9. Blood-based biomarkers

for early Alzheimer’s disease detection

- Market: Currently in its nascent stage and ready for clinical adoption

- Purpose/problem solved: Provides simpler, less invasive blood tests to detect biological signs of Alzheimer's disease potentially years earlier than current PET/CSF standards

- Key differentiator: Accessibility, potential lower cost, reduced patient burden vs. current standards

- Current adoption & scale: Low but growing clinical volume for new specific blood biomarkers (e.g., p-tau, Aß ratio tests) in specialized settings

- Adoption drivers: Massive and growing disease burden (~10M new dementia cases globally/year); aging populations; development of new drugs that require early diagnosis

- Commercial hurdles: Robust validation across diverse populations, establishing clinical utility/thresholds, regulatory approvals, reimbursement coverage

- Future potential: Positions Alzheimer's management toward earlier, proactive interventions, enabling preventive strategies and enrollment into disease-modifying clinical trials

10. Breath biopsy

- Market: US$ 2.2B (Global)

- Purpose/problem solved: Non-invasively analyzes breath (VOCs) to potentially detect diseases like lung cancer or monitor respiratory conditions

- Key differentiator: Completely non-invasive, simple collection, potential for frequent screening/monitoring

- Current adoption & scale: Minimal clinical volume; primarily confined to research and validation studies

- Adoption drivers: Strong appeal of non-invasive screening; potential applications across multiple high-burden diseases (e.g., lung cancer ~2.5M global cases)

- Commercial hurdles: Establishing reliable links between specific breath compounds and diseases; ensuring consistent results despite environmental factors (diet, air quality); developing robust, standardized collection and analysis methods; proving clinical accuracy

- Future potential: Could enable widespread, real-time disease screening and monitoring through simple breath tests, dramatically expanding preventive care and early intervention capabilities

Cross-cutting

strategic questions for leaders

These

innovations, while diverse, raise fundamental strategic questions that leaders

across the healthcare ecosystem must address:

- Value & access: How will we demonstrate clear clinical and economic value to secure regulatory approval, payer reimbursement, and clinician adoption?

- Integration: How must workflows, IT systems, and workforce skills fundamentally change to integrate these new diagnostics at scale?

- Business model: What new business models are needed for predictive, personalized, and decentralized diagnostics, and how do we build sustainable advantage beyond the technology itself?

- Investment strategy: How do we prioritize investments and partnerships across the diagnostics portfolio, balancing risk, return, and long-term strategic positioning?

- Data & trust: What data governance, analytics capabilities, and ethical frameworks are essential to manage complex diagnostic data while ensuring both innovation and trust?