Farmer centric innovation in animal feed

01 Aug 2025

The

global animal feed industry, long characterised by scale but low

differentiation, is undergoing a quiet transformation. Across emerging markets

like India and advanced economies alike, innovation focused squarely on farmers

is redefining how feed is produced, distributed, and consumed, with profound

consequences for rural livelihoods, supply chains, and agri-business margins.

Expanding

market, led by emerging economies

Globally,

the animal feed sector is projected to grow from an estimated US$ 483B in

2025 to more than US$ 600B by the early 2030s (Exhibit 1), registering a

compound annual growth rate of 5%. Asia-Pacific dominates the market,

accounting for nearly one-third of global production, driven by strong demand

from China, India, Vietnam and Indonesia.

India, in particular, is emerging as a key node. The country’s animal feed market comprising cattle, poultry, aquaculture, and pig feed is valued at US$ 14B in 2025, this will rise to US$ 20B by 2030 (Exhibit 1), growing at a CAGR of 7%. This is fuelled by a confluence of factors: rising protein consumption, policy support for animal husbandry, and a growing base of tech-savvy, productivity-driven farmers.

Exhibit 1: India's global animal feed market share & export performance

India’s

animal feed exports declined sharply in 2024, falling nearly 20% year-on-year after several

years of robust growth. Export values had risen from US$ 1.5B in 2020 to a peak of US$ 3B in 2023, before dropping

to US$2.3 billion

in 2024. Despite the recent dip, the sector still recorded a healthy 12% CAGR over the 2020–2024

period. Bangladesh remained the

largest export destination, followed by Vietnam, South Korea,

Iran, and Nepal indicating sustained regional demand despite tightening supply.

The export decline was primarily driven by a 21% fall in oilmeal shipments in FY25, stemming from both policy constraints and weakening external demand. A key regulatory factor was the government’s ban on de-oiled rice bran (DORB) exports, implemented in July 2023 and extended through September 2025. DORB, which previously accounted for 10–12% of total feed exports, saw volumes fall to near zero.

Concurrently, demand for soybean and rapeseed meal weakened across key Asian markets, further reducing outbound volumes.

Domestically, surging consumption by the poultry, dairy, and ethanol sectors has further tightened exportable supply. The poultry and dairy industries, which together consume over 80% of India’s compound feed, are expanding steadily. Broiler production has been growing at 7–8% annually, while milk output rose by 5.3% in 2022–23. These segments are heavily dependent on protein-rich inputs like soybean meal, rapeseed meal, and DORB.

Simultaneously, the ethanol blending programme which targets 20% blending by 2025 has diverted an estimated 5–6 million tonnes of grains (notably maize) from feed to fuel, creating further input shortages and upward pressure on prices.

This growing competition for feed raw materials within the domestic market has reduced India’s exportable surplus, even as global markets remain volatile. With rising domestic costs and limited inventory, India’s ability to offer competitively priced feed exports has weakened particularly against low-cost producers like Argentina and Brazil. As a result, India has lost market share in key oilmeal importing nations such as Vietnam and South Korea, underscoring its declining competitiveness in a saturated global feed landscape.

Despite recent headwinds, India remains well-positioned to expand its footprint in global feed markets. As global buyers diversify supply chains and seek cost-effective alternatives, India’s scale, proximity to key Asian markets, and evolving trade architecture may help it capture greater market share in the coming years.

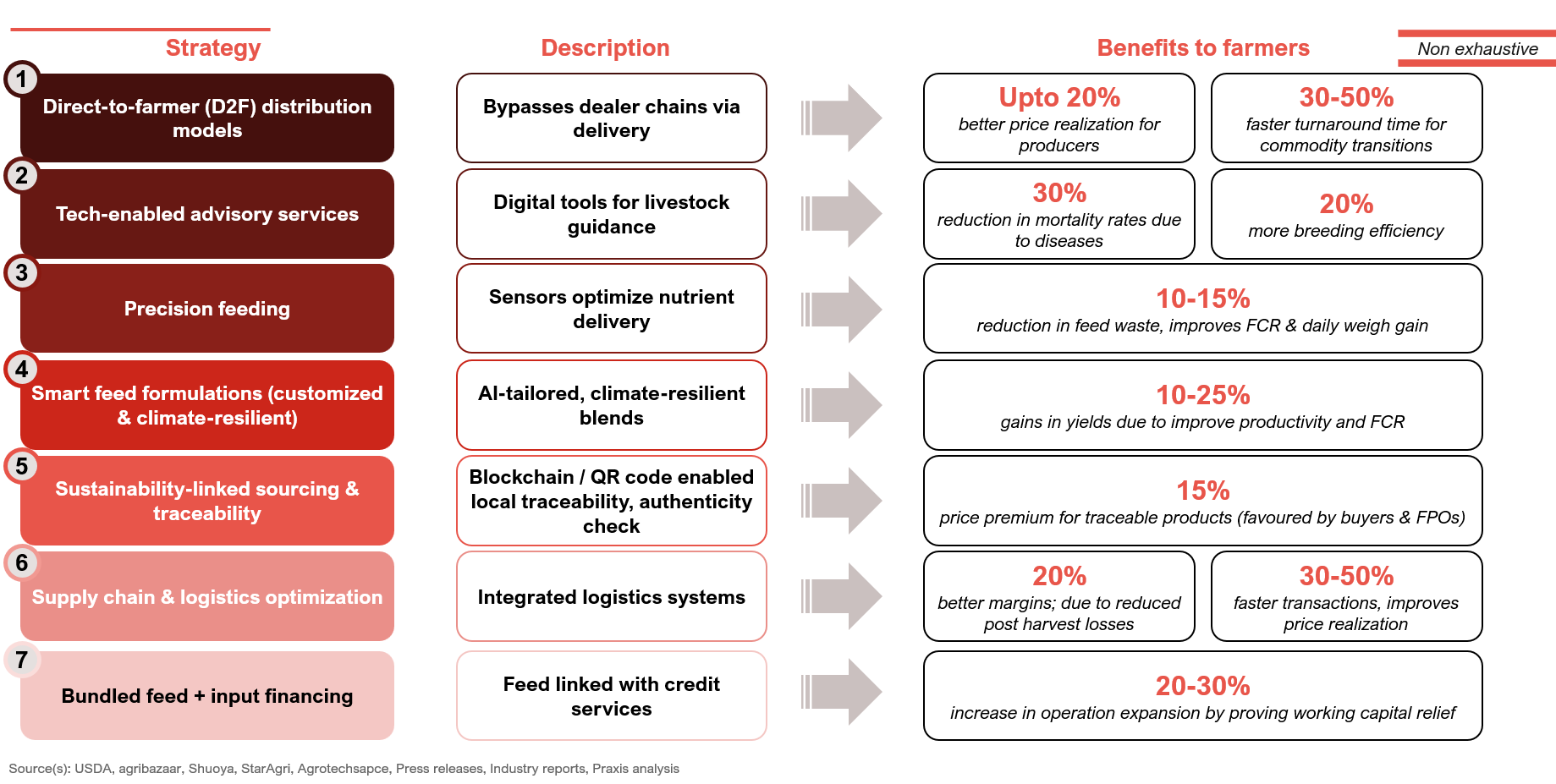

Corporate strategy turns farmer first

In

India, feed companies traditionally focused on scale and logistics are now

pivoting to a farmer-first model, investing in technology, advisory platforms

and custom formulations (Exhibit 2).

Exhibit 2: Corporate strategies

pivoting to farmer-first models

Globally newer players are challenging conventional market working:

Charoen Pokphand Foods (CPF), the Thai conglomerate, has expanded its feed-tech R&D capabilities, with a focus on traceability and efficiency. CPF’s digital solutions allow farmers to monitor animal weight gain and feed conversion in real time, linking feed consumption directly to yield and margins.

In the UK, start-ups are building modular systems where Black Soldier Fly (BSF) larvae consume organic waste and are then proceeded into high-protein insect meal (upto 60%). This sustainable feed alternative to soy and fishmeal is gaining popularity in poultry and aquaculture. With lower land, water, and emissions intensity, and reduced logistics cost, BSF based systems align with circular economy goals and are drawing investor interest amid tightening sustainability norms.

From

productivity gains to profitability uplift

Feed

innovations are delivering measurable impacts at the farm level translating

directly into both productivity improvements and profitability gains.

In poultry, the adoption of phytogenic additives, amino acid fortification, and digital advisory tools has led to a 12% increase in average daily weight gain, along with marked improvements in feed conversion ratios (FCR). These efficiency gains are driving net income increases of INR 7-12 per bird, varying by farm size across small, medium, and large-scale operations.

In dairy, especially in heat-stressed regions (like Maharashtra), enhanced feed blends have boosted milk yields by 8–15%, helping farmers maintain performance under climatic stress.

Overall, these feed innovations result in:

- Shorter production cycles

- Lower input costs per unit of meat or milk

- Greater marketable output and improved profitability

The animal feed industry may never achieve the glamour of precision agriculture or biotech. But it is, quietly, becoming a battleground for innovation with real impact.

As regulatory pressures around traceability and sustainability intensify, and as global protein demand continues to climb, companies that prioritise farmer outcomes through better yield, health, and profitability are likely to capture the next phase of growth.

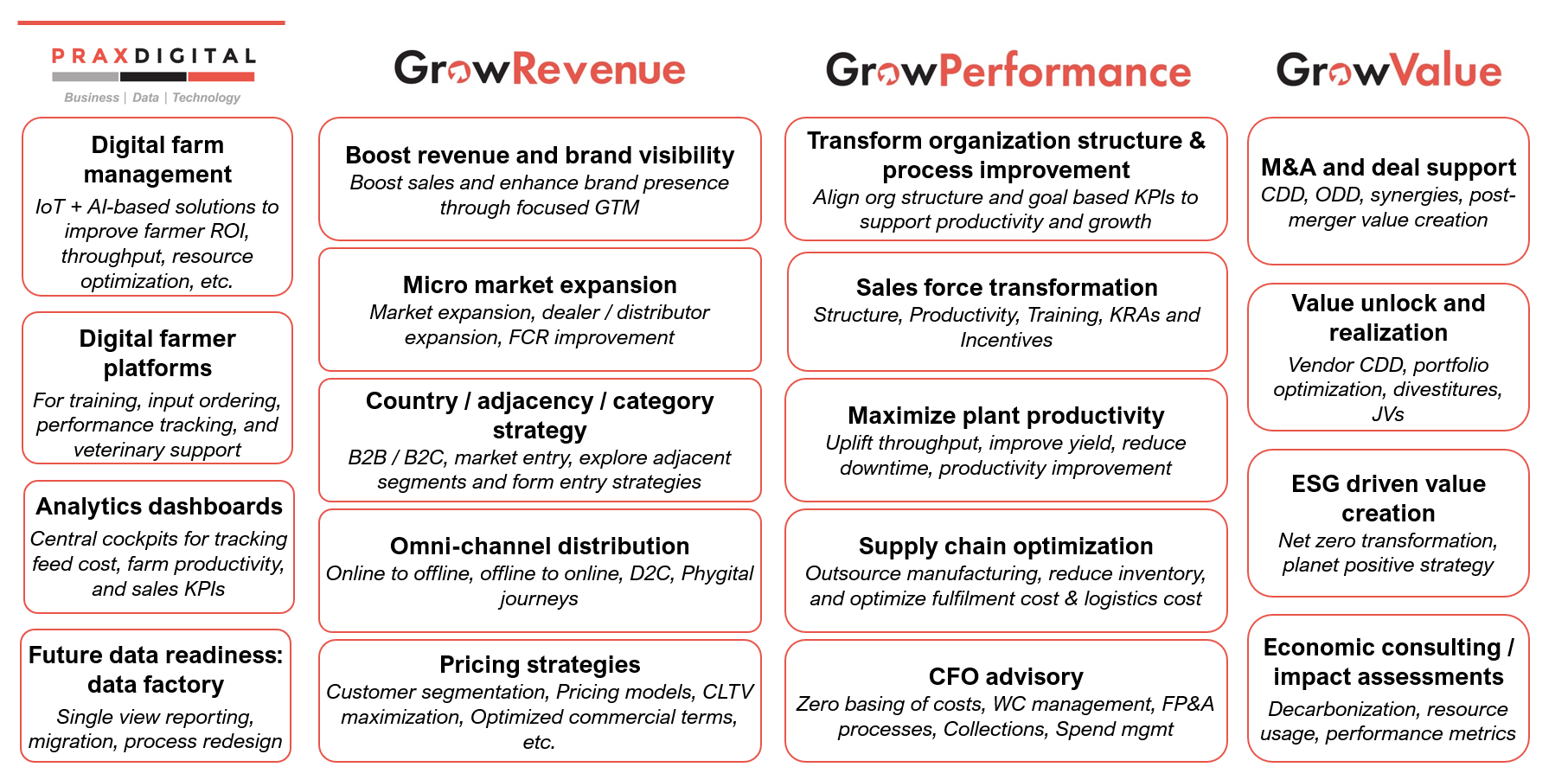

Exhibit 3: Capabilities we build and implement